Last fall, Pennsylvania lawmakers set out to fix a problem

with the state’s 2004 Alternative Energy Portfolio Standards Act (AEPS).

No, the problem they took on with Act 40 of 2017 was not the weakness of the renewable

energy targets in the AEPS. (Those targets still have not been updated since 2004). Act 40 addressed the “oversupplied” state of Pennsylvania’s Solar Renewable

Energy Credits (SREC) market. Before Act 40, the AEPS gave solar projects

located throughout the PJM

region (which stretches as far west as Illinois and as far south as

North Carolina) the unqualified right to sell SRECs in Pennsylvania. The

resulting glut of SRECs led to depressed SREC prices, which has made solar

development less economical in the state. Act 40’s fix was to establish new,

more restrictive SREC eligibility criteria in order to spur more in-state solar

photovoltaic (PV) development, and thereby deliver more clean air benefits to

Pennsylvanians.

So far, so good. But in December 2017, the Pennsylvania

Public Utility Commission (PUC), which will administer Act 40, proposed an

interpretation of the law that would completely undermine its purpose. As a

legal matter, the PUC’s interpretation is mistaken. Practically speaking, the

controversy over Act 40’s construction underscores the need for Pennsylvania to

strengthen the solar (and other renewables) targets in the AEPS. If they were

stronger, Act 40 might not be needed at all.

The solar PV target in the AEPS is 0.5% of retail

electricity sales in 2020, a goal that Pennsylvania has been slowly inching

toward since 2006.

Electricity distribution companies (i.e., utilities) and

electricity generation suppliers (EGS) meet these targets by buying SRECs

generated by qualified solar projects. (Each SREC represents 1 MWh of

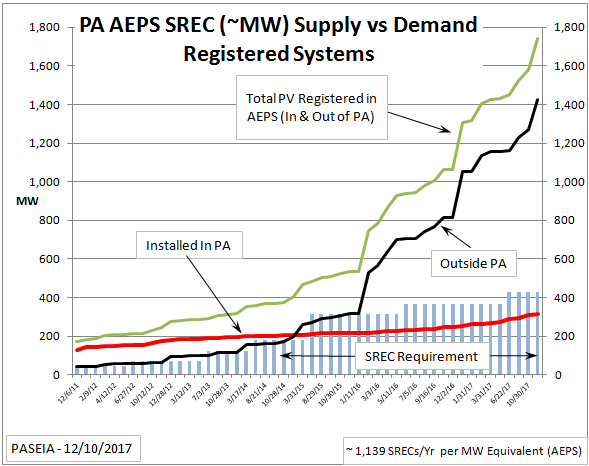

electricity). Between the smallness of the solar PV targets in the AEPS and the

large number of SRECs that have poured into Pennsylvania’s Alternative Energy

Credit market (in 2017, more than 60% of all the SRECs purchased for AEPS

compliance came from outside Pennsylvania), the market is “oversupplied” –

i.e., there are more SRECs for sale than utilities and EGS need to buy.

As a result, SREC prices have plunged from more than $300.00/MWh in 2010 to less

than $5.00/MWh today. These low prices make solar development in Pennsylvania

harder, because solar projects are financed partly through the revenue stream

their SRECs will generate.

Act 40’s Fix

Act 40’s solution to this problem was to establish more

restrictive criteria for solar PV projects to sell SRECs in the Pennsylvania

market. Under Act 40, a solar project must (1) deliver electricity to the

customer of a Pennsylvania electric utility, (2) be connected to an electricity

distribution system operated by a Pennsylvania utility, a Pennsylvania

municipal electric system, or a Pennsylvania electric cooperative, or (3) be

connected to a transmission system located within the service area of a

Pennsylvania utility.

According to State Sen. Mario Scavello, R-40, the author of

Act 40’s solar provisions, the intent of

the law is that “out-of-state systems will no longer qualify” to sell SRECs in

Pennsylvania’s market, so that “[e]lectric distributors will now have to

purchase their credits from within the commonwealth.” Similarly, Gov. Tom

Wolf, D-Pa., touted his signing of Act 40 as a way of “making sure that

the benefits of increased renewable jobs, a cleaner environment, and a growing

renewable economy will be felt in the commonwealth.” Expanding solar

energy, the governor added, “is incredibly important to

Pennsylvania’s carbon footprint and demonstrates our state’s commitment to

leadership on the most important environmental issue confronting the world.”

The PUC’s Misinterpretation of Act 40 (and an Alternative

Interpretation)

Although the clear intent of Act 40 is to exclude

out-of-state solar PV systems from Pennsylvania’s SREC market, the PUC’s

Tentative Implementation Order (TIO) for Act 40 proposed to “grandfather” such

systems into the market because of the following language:

Nothing under this section … shall affect … a certification

originating within the geographical boundaries of this Commonwealth … of a

solar photovoltaic energy generator as a qualifying alternative energy source

eligible to meet the solar photovoltaic share of [the AEPS].

According to the TIO, this section requires the

grandfathering of all solar PV systems previously “certified” for

Pennsylvania’s SREC market – regardless of location – on the grounds that the

administrative act of certifying them took place inside the state. But as comments

submitted by us at the Natural Resources Defense Council (NRDC)

and several other environmental organizations point out, the TIO’s

interpretation is untenable, among other reasons because it ignores legislative

intent and strips the phrase “within the geographical boundaries” or any

meaning.

Fortunately, PUC Chairwoman Gladys Brown and Vice Chair

Andrew Place have proposed an alternative

reading of this language. Recognizing that Act 40 does not define

“certification” and acknowledging the clear intent of the General Assembly,

Brown and Place would read a certification as originating in Pennsylvania only

when the solar system being certified is located in Pennsylvania. NRDC, as well

as Senator Scavello and other legislators, have urged the full PUC to embrace

this interpretation, which would grandfather only Pennsylvania solar systems.

What’s Next?

The PUC’s public comment period on the TIO and the

alternative interpretation offered by Chairwoman Brown and Vice Chair Place

ends on Feb. 5. After that, the PUC will issue a final Implementation Order. If

the PUC interprets Act 40 consistent with legislative intent, it will provide

Pennsylvania with an economic and environmental boost, especially if the

General Assembly and Governor Wolf go one step further and strengthen the

state’s clean energy standards.

Meanwhile, whatever the content of the final order, the

other factor driving low SREC prices in Pennsylvania – tepid demand, due to the

AEPS’ weak renewable goals – remains. Pennsylvania’s renewable energy industry

today supports nearly 10,000 jobs, and the state is home to more than 500 solar businesses. These businesses are

helping homes and businesses meet their electricity needs without harmful

greenhouse-gas emissions. With the AEPS set to plateau in 2021, the state needs

to set more aggressive, long-term targets to realize the economic and

environmental potential of solar energy in Pennsylvania.

No comments:

Post a Comment